New FinTech platforms have played a critical role in recent years in improving financial inclusion in Africa. This trend is set to continue with their growth potential unlocking greater economic prosperity.

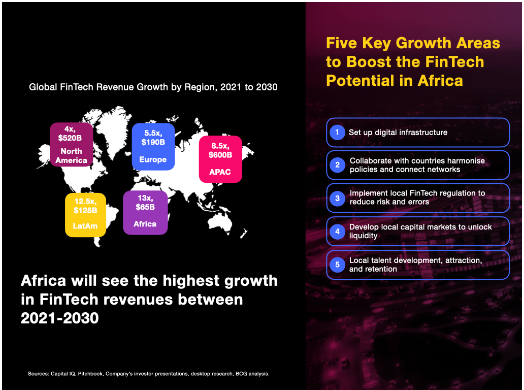

Nairobi / Lagos / Accra , 15 November 2023 -/African Media Agency (AMA)/- Africa is one of the fastest growing FinTech markets with revenue forecasted to grow 13 fold to $65-billion by 2030. In addition to the revenue opportunity, FinTechs play an important role in developing the region’s economy and improving the lives of African people by revolutionising the financial sector.

Two new reports from Boston Consulting Group (BCG), in collaboration with Elevandi, highlight how to further advance financial inclusion on the continent and explore advancing the FinTech industry and unlocking its full potential in the years to come.

The first report, Driving Financial Inclusion in Africa, unpacks the growth of financial inclusion in Africa since M-PESA was founded in Kenya in 2007. While some large economies (South Africa, Kenya, Uganda and Ghana) have made significant progress in financial inclusion, there is still a long way to go and significant opportunity which supports the continuous high investment in African FinTechs.

“The first wave of FinTechs, driven by mobile money and payment solutions have already enabled a step change in financial inclusion and trust in digital solutions. A second wave of FinTechs with a wider product offering can now leverage the platforms created to access a broader population and further accelerate financial inclusion,” says Caio Anteghini, partner at BCG, Johannesburg.

The report also explains the different business models that FinTechs can thrive in, in this context, and while many of them are disrupting the financial sector, there are several opportunities for collaboration between incumbent players and FinTechs. Forty percent of African FinTechs are focused on digitally enabling existing financial institutions instead of competing against them.

Driving further financial inclusion

The report suggests that payments and lending will be the drivers of further financial inclusion, and the key areas of investments in the coming years.

Payments FinTechs were the first movers representing 45% of companies pre-2013. This segment is yet to reach its full potential by continuing to solve for critical African pain points such as financial inclusion and the high cost of transactions.

Lending will join forces with growth centered around microfinance, a great enabler of financial inclusion.

Local businesses need basic credit for day-to-day activities and capital investments but often don’t have the tools or credentials to go through traditional channels. For FinTechs, it makes sense to focus on this small to medium-sized enterprise (SME) segment due to the sizes of loans, broader scale, and financial transparency. One example of successful microlending is JUMO World, which is building banking infrastructure with a focus on assessing the credit worthiness of SMEs.

The report finds that FinTechs enabling financial institutions (41% of active firms) receive more funding on average (49%) than those that adopt disruptive business models (59% of active firms receive 51% of funding), indicating a shift in the ecosystem.

Additionally, the report proposes four winning strategies for FinTechs and the appropriate support governments could provide to enable them to flourish. FinTechs providing specific services via existing platforms, distributing a fully-fledged solution via existing platforms, creating a new platform starting in niche segments, and B2B solutions could lead to the next wave of growth for incumbents and new entrants.

“Policymakers can be a huge catalyst to the FinTech industry by developing the infrastructure and favourable regulatory environment,” says Pat Patel, Executive Director of Elevandi. When it comes to specific applications for improving financial inclusion, they can further support advancements by acting in four areas: Awareness campaigns to increase literacy, institutional support and investment, and launching data-sharing platforms to lay the foundation for platforms. Unlocking funding will also aid advancements in financial inclusion.

On top of the infrastructure created in the first wave, greater adoption of smartphones, better connectivity, and cloud adoption in front-running countries will be instrumental to the second wave of growth.

Unlocking potential and funding

In the second report, Unlocking the FinTech Potential in Africa, BCG and Elevandi examine the benefits that FinTech has brought to Africa and the business models that FinTechs and investors need to create to scale up activities.

Almost half of the 1 000 FinTechs in Africa were founded in the past six years. Cumulatively, they have raised about $6-billion in equity financing since 2000, with investment growing at an incredible compound annual growth rate (CAGR) of 57% versus 27% for the rest of the globe.

At the same time, the African FinTech ecosystem is still nascent, with approximately 80% of rounds since 2018 at seed- or angel-level maturity. “This shows that the African market is already an attractive ecosystem to new entrants capturing a share of the unserved or underserved segment. However, to continue attracting new entrants, FinTechs must be able to scale across Africa, and not solely exist in siloed markets,” adds Patel.

Few FinTechs have been able to do so in the continent, where just 4% have reached series C funding or beyond, versus 11% for the rest of the world. The report suggests that investors and FinTechs need to address three key challenges to attract funding – identify an economically viable model that caters to African-specific challenges and is affordable, can scale beyond its home market given relatively small market sizes, and mitigates risks inherent to the developing continent.

Current FinTechs are heavily centred in Africa’s largest economies, with approximately 63% of all companies located in South Africa, Nigeria, Kenya, and Egypt and nearly 80% of funding flowing into these markets. To successfully move across borders, these companies will need to invest in understanding regulation, procure the appropriate licenses, likely adapt their business model, and develop a team on the ground to successfully execute their value proposition in the new market.

“FinTechs have been playing an important role in driving financial inclusion and economic development in their home countries. With the development of digital infrastructure and policy clarity and harmonisation, they will be able to extend their impact both in their home country and cross-border, and benefit even more people across the continent,” says Anteghini.

This growth does depend on key changes as FinTechs and investors face several hurdles, including high costs and different regulations in each jurisdiction. The report highlights five areas in particular that require attention: digital infrastructure, policy harmonisation, policy clarity, developing local capital markets and growing the local talent pool.

In recent years, the war for talent has intensified and Africa is struggling as some of its top talent has moved overseas tempted by higher salaries. At the same time, attracting foreign talent is difficult due to long, stringent visa procedures and lower liveability scores. It is crucial to reverse these trends, however, as the African education system is likely to only produce 50% of the skilled workers it requires. FinTechs have demonstrated their ability to succeed throughout the first stages of a company life cycle, but further scalability is unfeasible with current supply.

The high unbanked and underbanked population, accelerating mobile and internet penetration, and an increasing need for financial inclusion across the region present a great opportunity for FinTech companies. If policymakers can foster the right environment for FinTechs to grow and financial inclusion to expand, it will ultimately foster long-term financial inclusion, efficiency, and quality of life, which will turn into taxes, economic growth, and capacity to reinvest.

Download the reports here.

Distributed by African Media Agency on behalf of BCG.

About BCG in Africa

BCG has a strong and longstanding presence in Africa, with five offices across the continent supporting societal impact by helping organizations better anticipate and react to economic, social, environmental, and regulatory changes on the continent. BCG supports a wide variety of clients in the public sector, social sector, and private sector, and covers a spectrum of topics including digital transformation, climate and sustainability, technology, and innovation, and strengthening health and food systems.

About Elevandi

Elevandi is set up by the Monetary Authority of Singapore to foster an open dialogue between the public and private sectors to advance FinTech in the digital economy. Elevandi works closely with governments, founders, investors, and corporate leaders to drive collaboration, education, and new sources of value at the industry and national levels. Elevandi’s initiatives have convened over 350,000 people to drive the growth of FinTech through events, closed-door roundtables, investor programs, educational initiatives, and research. Elevandi’s flagship product is the Singapore FinTech Festival alongside fast-rising platforms, including the Point Zero Forum, Inclusive FinTech Forum, Japan FinTech Festival, Elevandi Insights Forum, The Capital Meets Policy Dialogue, The Founders Peak, and Green Shoots. Visit www.elevandi.io to learn more about Elevandi.

The post Continued growth of Africa’s FinTechs can unlock greater economic prosperity appeared first on African Media Agency.